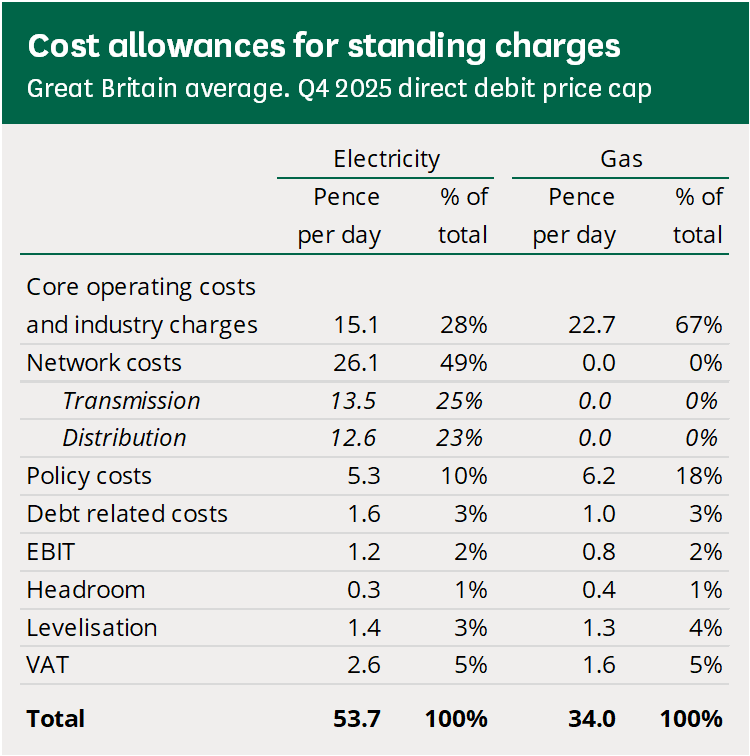

Suppliers do have some flexibility over where they can recover different costs. Analysis by the research foundation Nesta has shown that a significant share of electricity network and policy costs are recovered through the standing charge rather than the unit rate.

Why have they risen so much in recent years?

The shift has been dramatic. Between 2021 and 2023 it was found that the average standing charges had more than doubled and have further increased since then.

The main causes for these rises have been:

Post-crisis cost recovery: Supplier failures, customer debt and the cost of emergency support schemes created significant fixed costs that regulators allowed suppliers to spread through standing charges.

Network upgrades: Keeping ageing networks running is expensive. The existing networks weren’t prepared for the increasing % of energy derived from renewable sources and needed a rapid update. This was partially down to the short-sightedness of government policies forcing more widespread renewable energy usage.

Risk management for suppliers: Recovering more income through a fixed fee gives suppliers a more predictable cashflow than relying solely on units sold -- especially when wholesale prices are volatile.

The result is that low-usage businesses, who were previously able to save more by cutting consumption, now see less benefit because a larger part of the bill remains unmoved.

Are they set to keep rising?

Looking ahead, there are two key factors likely to dictate how standing charges change

On one side, Ofgem has signalled massive new investment in energy networks -- around £24 billion between 2026 and 2031 -- which it estimates could add around £100 a year to typical bills (but far more for large businesses) by 2031 in order to fund grid upgrades. In recent years, these have been exactly the sort of fixed system costs that end up in standing charges.

On the other side, there’s growing political and consumer pressure to reduce these charges. Ofgem has now confirmed that by early 2026, suppliers will have to offer at least one tariff with a lower standing charge, even if that means a higher unit rate. Although, this will be more targeted at domestic users rather than low-consuming businesses.

While it doesn’t seem likely that standing charges will drop in the near future, the pressure from end-users will likely lead to more choice regarding how much of their energy costs are made up of fixed charges. For smaller consumers, there will be a greater benefit in being able to choose a lower standing charge with higher unit rates should these offerings become standard throughout the industry.

If your business would like more information on standing charges or any of the charges that appear on your bill, don’t hesitate to contact SeeMore Energy today. Our experienced advisors can help you with bespoke strategies and advice that is tailored to your needs.