Prices did drop shortly after this but would then mostly trade in a tight range as prices remained propped up by EU mandated purchasing -- designed to ensure that all EU nations possessed sufficient gas reserves ahead of this winter. With that purchasing cycle now complete, we are seeing wholesale prices once again drop, with prices at the end of Wednesday (10/12/25) being their lowest since April’24.

Why are prices falling?

- An Easing of EU Buying Pressure

As previously mentioned, the EU mandated reserve levels have forced many nations to make purchases throughout the summer months. The deadline for EU nations to achieve the required % of gas reserve capacity has now passed, removing buying pressure from the market

- Russia-Ukraine Peace Talks

Since the beginning of 2025, the EU banned the importation of Russian gas. This narrowed the available suppliers that European nations could purchase from. However, with active peace talks taking place there are hopes this decision could be reversed. It is seen as inevitable that the embargo being lifted would be a prerequisite ahead of Russia signing any peace deal. This would create a more competitive supply picture that would favour the buyers.

The US made significant increases to the amount of LNG they are exporting during the course of 2025. With further production and export increases expected early in 2026, this has reshaped the supply vs demand balance. 56% of the LNG imported to Europe this year has come from US, meaning that European nations are less reliant on supplies from nations like Qatar where issues surrounding shipping routes had previously elevated prices.

Whilst weather forecasts are never 100% reliable, recent indications have suggested that the UK winter weather will be milder than usual, particularly after December 17th. With the supply side of the equation currently looking healthier than in recent memory, news that demand may also be reduced only further assists prices in their decline.

What this means for your business

Wholesale prices can sometimes have a slight delay before they are directly observable in the prices available to end users. With the most recent decline beginning on November 20th, we are now beginning to see this affect the unit rates available from UK suppliers.

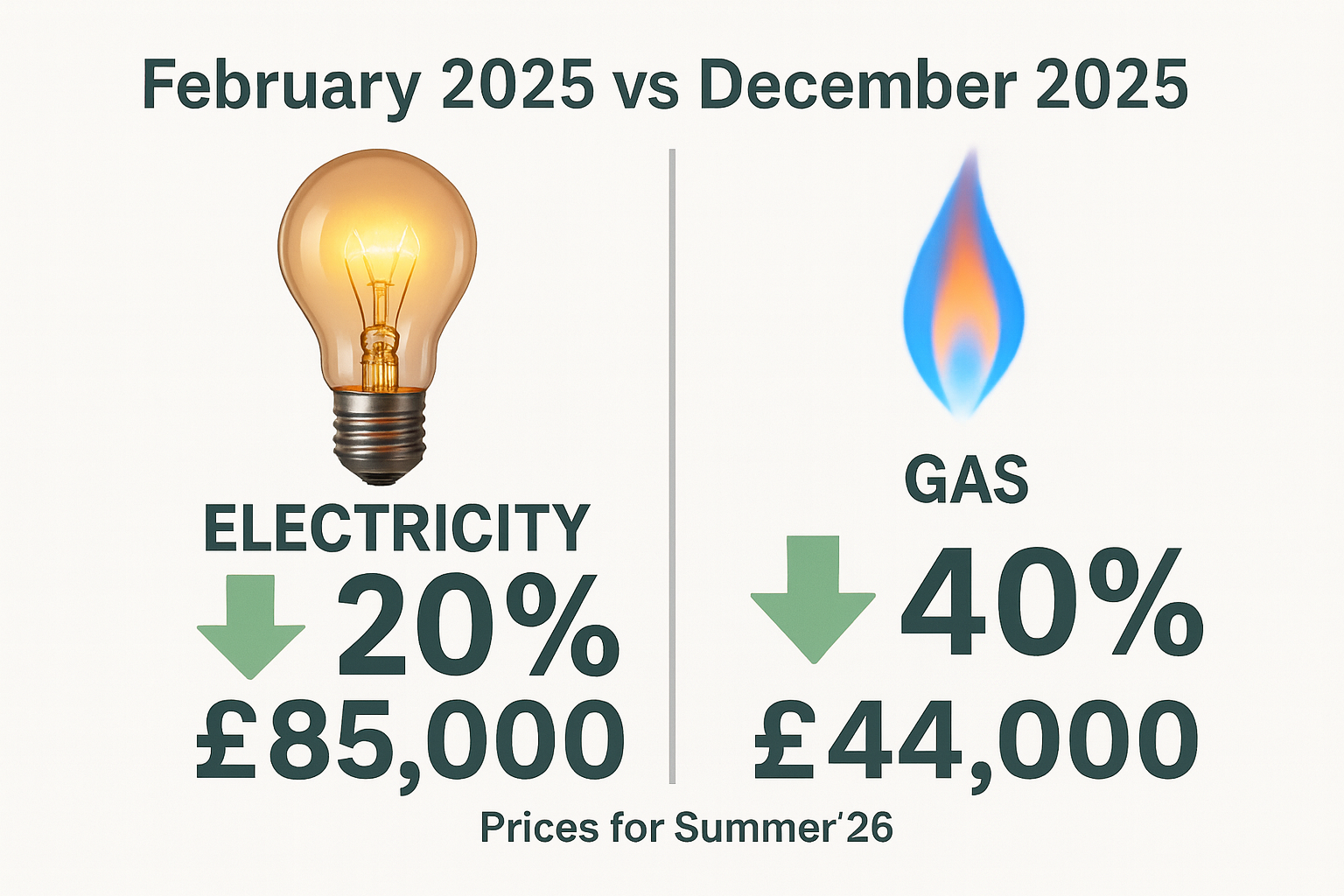

Prices for Summer’26 electricity are now over 20% lower than they were during February of this year, with gas prices now 40% lower for the same periods. For a business that is set to consume 5,000 MWh of electricity and 1,000 therms of gas during this period, this represents

a saving of approximately £85,000 on the electricity and £44,000 on the gas.