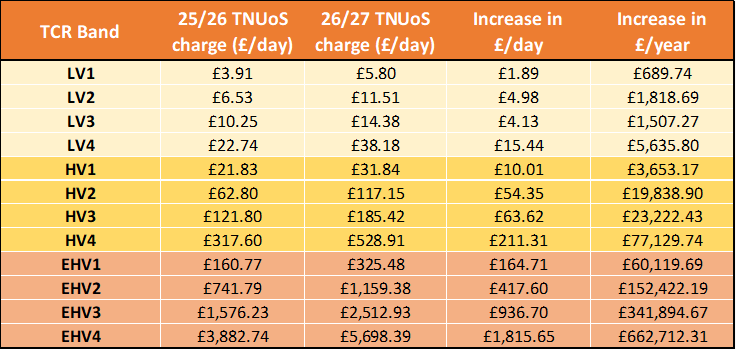

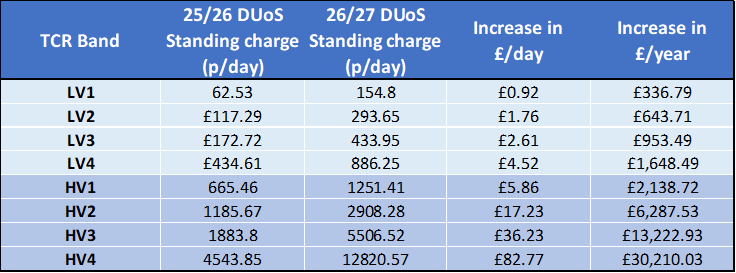

DUoS charges for EHV meters are dependent on the MPAN and not the band. Let us know if you require assistance with checking the charges of your EHV meters.

What this means for British businesses

A mid-sized factory with a high-voltage connection could be looking at

between a £26,000 - £107,000 increase regardless of changes in their consumption.

For businesses already dealing with tight margins, global supply chain pressures, and rising labour costs, these increases can have a big impact on profitability. Especially when -- for the majority of businesses (depending on the contract) -- they are applied automatically via supplier pass-through mechanisms.

What You Can Do Now

While network charges may seem uncontrollable, there are steps that businesses can take to mitigate their impact:

1. Assess your TCR banding. Many businesses are unknowingly placed in higher DUoS or TNUoS bands. A misclassification of bands could cost your business thousands every year. We can help you audit your current setup, see if changes can be made, and challenge incorrect allocations.

2. Review your kVA capacity. For many businesses, a

kVA capacity review can save thousands per year and possibly move your meter into a lower TCR band

3. Explore demand flexibility and onsite generation. Where possible, shifting load to off-peak periods or investing in onsite renewable or storage solutions can reduce chargeable capacity and unit costs.

Network costs are no longer a small part of your energy bill. With DUoS and TNUoS costs rising sharply from

April 1st, 2026, businesses can act now to see what can be done to mitigate these charges.

We specialise in helping businesses navigate complex energy cost structures, optimise their billing, and put in place tailored strategies that help reduce energy spend. If you would like help with any of the issues mentioned in this article, contact us today to see how our team of experts can help you ahead of these rising charges.