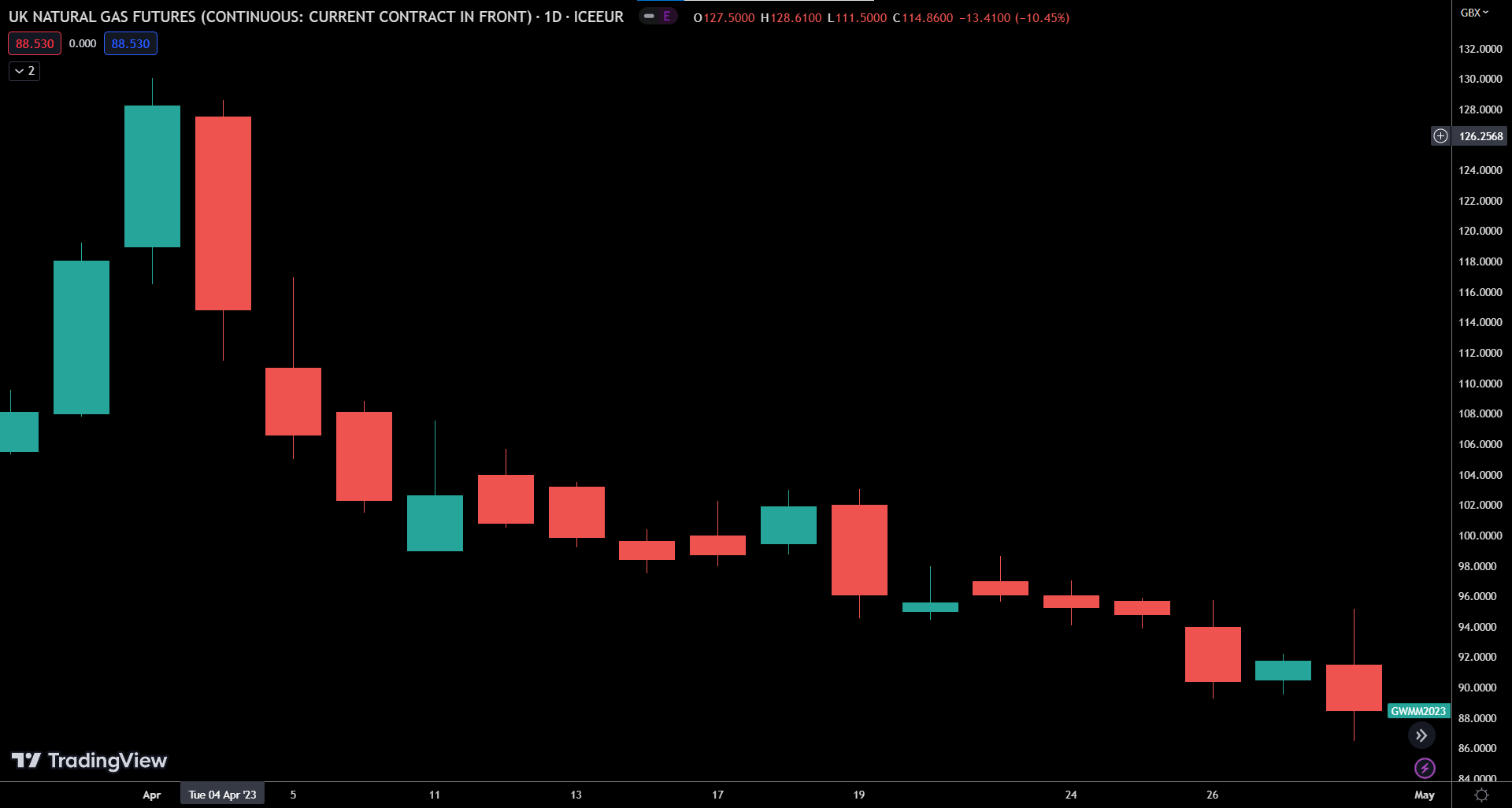

October Review By Adam Novakovic In the month of Halloween, October energy price movements were free of jump-scares. Whilst prices moved up slightly at the start of the month, they marginally decreased throughout the remainder of October. Ending the month slightly below the levels seen at the end of September. The expectation this month was that European gas reserves would be the key story impacting energy prices. The European Network for Transmission System Operators for Gas (ENTSOG) released their report on the Winter supply outlook. This confirmed that Europe is well prepared for the coming winter, with 83 % gas reserves recorded as of the 1st of October, and infrastructure resilient enough to meet demand without Russian pipeline gas. Their projections had Europe ending the winter season with over 30% storage even in the most severe scenarios. There is also the expectation that any unforeseen supply disruptions can be mitigated through increased LNG imports -- supporting the EU’s goal of phasing out Russian gas while emphasising continually reducing demand. During the first week of October Russia launched a wave of drone attacks against Ukraine -- the largest since the war began. These strikes have damaged Ukrainian gas production and left storage at 42% of capacity. This has forced Ukraine to look at importing large quantities of LNG from Europe this winter. With the deal that brought Russian gas to Europe now expired, Europe faces added demand pressure. This comes despite Europe significantly reducing Russian gas imports and increasing LNG imports from other nations. With there currently being a large quantity of LNG available for importation, and with EU gas reserves being in a healthy position, it seems as though further conflict may not have a large impact on energy prices. This could change however if Europe were to experience a particularly cold winter.

September Review By Adam Novakovic We have reached the time of year where the summer months have started to fade and we begin to think about the colder seasons. This month saw the UK government recognise Palestine as a country, although they still seem unable to recognise the harm their energy policies are causing UK businesses. With further charges set to be added to UK energy bills and rising non-commodity costs, it was a relief that wholesale energy prices remained fairly flat throughout September. A recent report from independent analysts Cornwall Insights revealed that large energy users who aren’t covered by Government schemes could find that they are paying a further £450,000/year in non-commodity costs by 2030. With non-commodity costs such as DUOS and TUOS charges –which are used to fund the infrastructure responsible for the transmission of electricity – now accounting for over 2/3rds of total electricity costs for some businesses, it is of growing concern that these charges are set to continue rising. With the TUOS charges for 26/27 expected to increase significantly , the non-commodity charges are starting to have a negative impact on UK businesses ability to compete against foreign businesses with fewer governmental charges on their energy bills. This growing concern is yet to be addressed but could have a huge impact on many industries in the next year.