One factor which could keep prices high after the negotiation of a peace deal would be European nations looking to refill their gas reserves. While many nations now have much stronger renewable energy production than ever before, EU mandates will still force strong buying behaviour from all member states. With a limited global availability of LNG, this could lead to bidding wars for the available cargoes.

There have been suggestions that US LNG can plug some of the gaps in the market, but assuming an increase to maximum possible production capacity and the shifting of some cargoes from Asia to Europe, it may only make up a third of the shortfall. One possibility which could have a large impact, would be if sanctions were to be lifted against Russian gas. While many European nations have been vocal against this, the situation has changed and the US lifted embargoes against Russian oil in the early part of March, setting an international precedent.

A detail that may limit the upside from rising LNG prices, is that wind is now responsible for generating over 25% of UK electricity. Whilst wind lacks the reliability of other sources, this does change the energy-generation landscape compared to previous energy crises. Previously a higher % of generation was dependent on gas and coal, but renewable energy production – while lacking the reliability of gas or nuclear energy generation -- offers some relief from this burden.

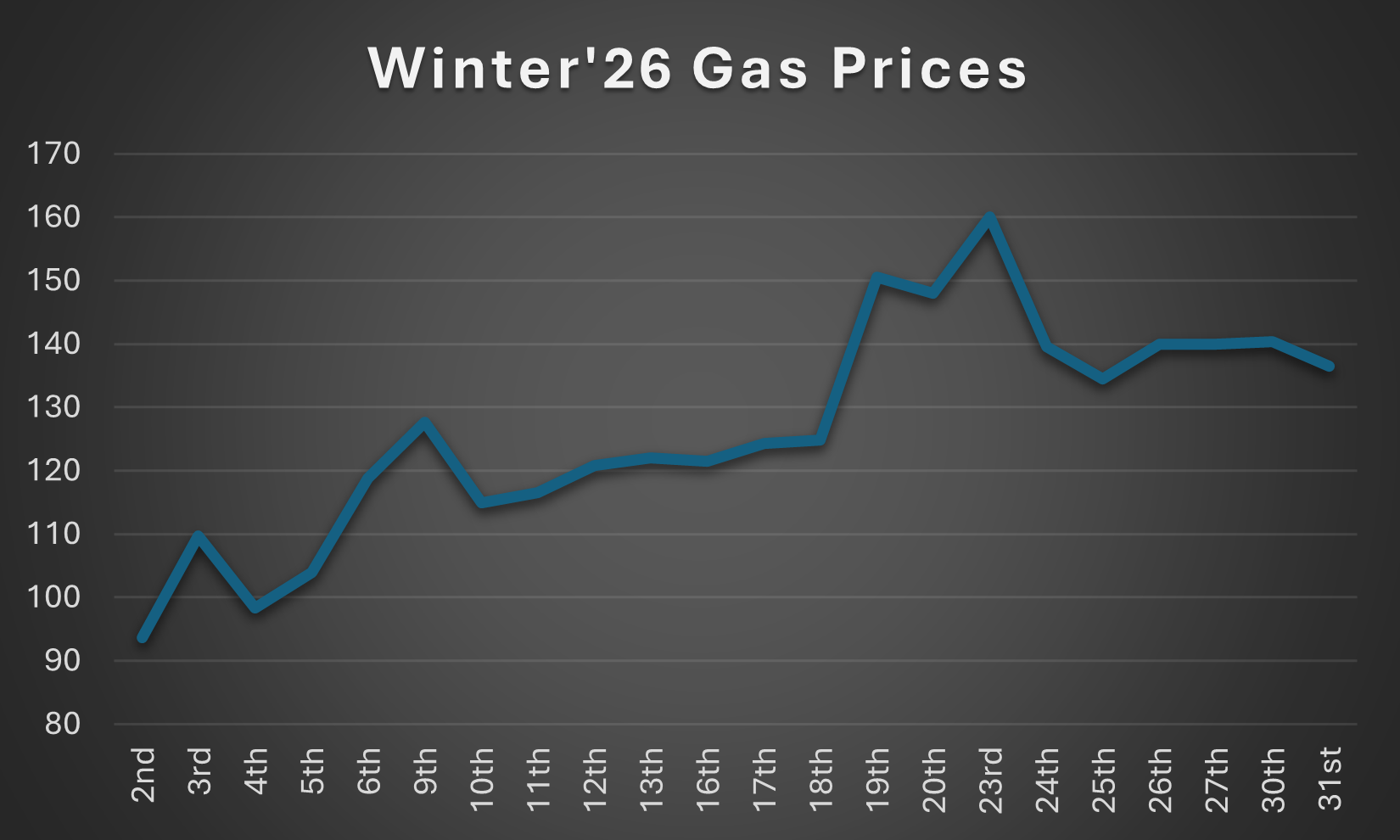

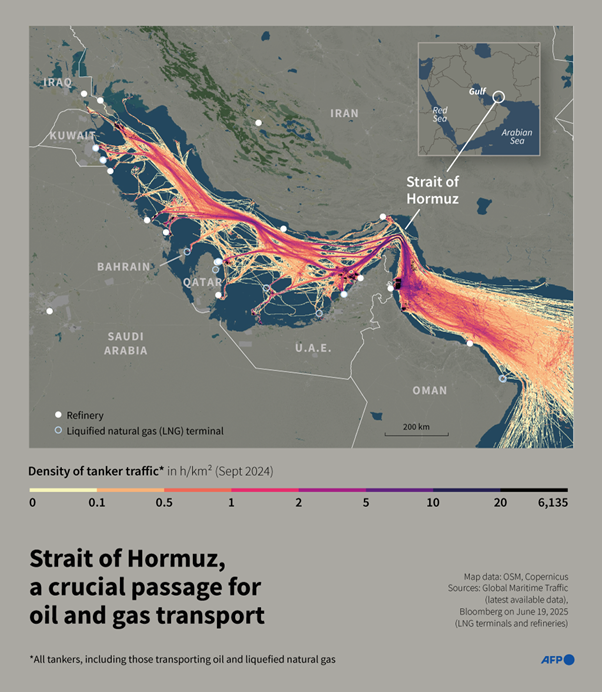

In the coming months, the re-opening of the Strait of Hormuz will be the most important factor impacting energy prices, with a hasty re-opening potentially limiting how long prices will remain inflated.

With prices at their current levels, this has created issues for many British businesses, if you have been affected by the rising energy costs, or if you have gas or electricity contracts set for renewal in the next 12 months, contact us today for free, professional advice on how to navigate the current volatile energy landscape.